August 19, 2025

In 2026, employers will face similar challenges as encountered in previous years, yet at a steeper trajectory and more severe impact. The survey results highlight the health care cost and delivery challenges confronting employers. Based on the findings of this survey, the following emerged as the top insights:

-

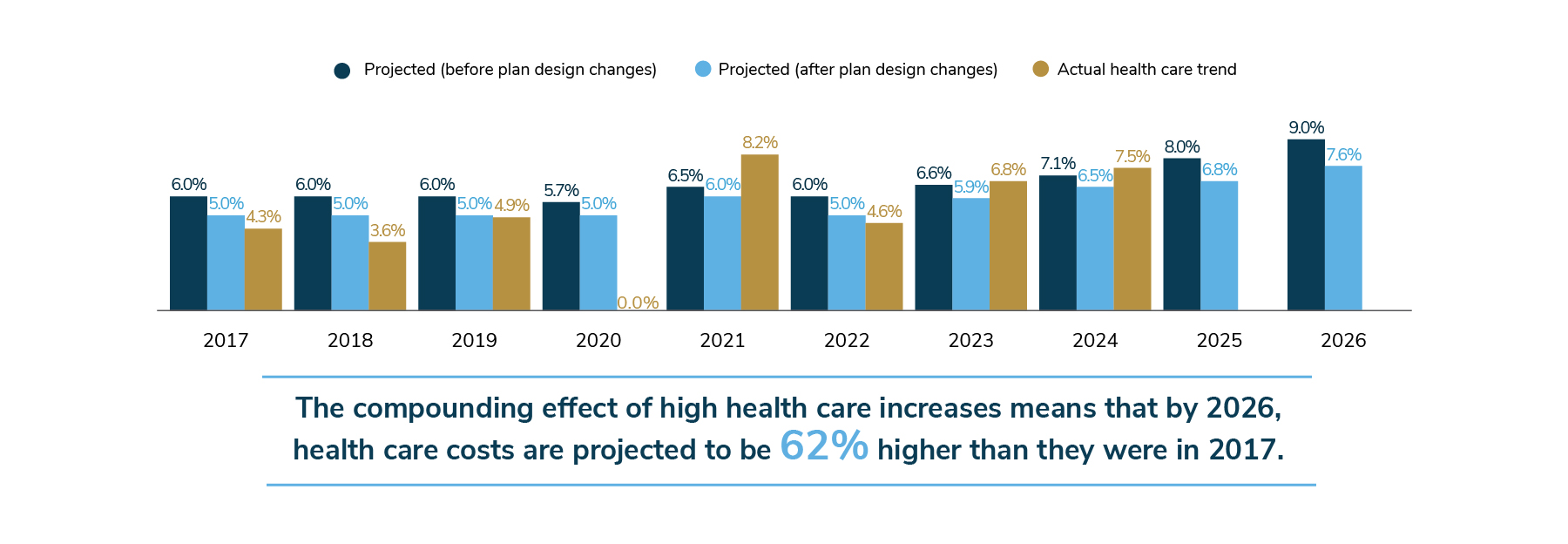

1 | Employers are facing steeper year-over-year health care cost increases, a development made clear after actual health care costs significantly exceeded employer forecasts for the second year in a row. This calls for employers to act with greater urgency than in the past.

In 2023 and 2024, employers experienced the highest back-to-back increases in a decade, surpassing what they had projected and budgeted for. As a result, employers started 2025 at a major cost disadvantage, likely adversely impacting how 2025 full year costs will end up relative to already high budgets for the year. Against this cost paradigm, employers predict that health care cost trend for 2026 will come in at a median of 9%, which falls to 7.6% with plan design changes. Understandably, employers say their top priority in the coming year is health care costs overall, followed by affordability for their organization and affordability for employees.

Figure 1: Median Health Care Trend (Actual and Projected), 2017-2026

Figure 1: Median Health Care Trend (Actual and Projected), 2017-2026 -

2 | While employers have always sought to adopt sustainable cost-containment approaches, the current unfavorable environment is a call to action for bolder moves to address health care costs.

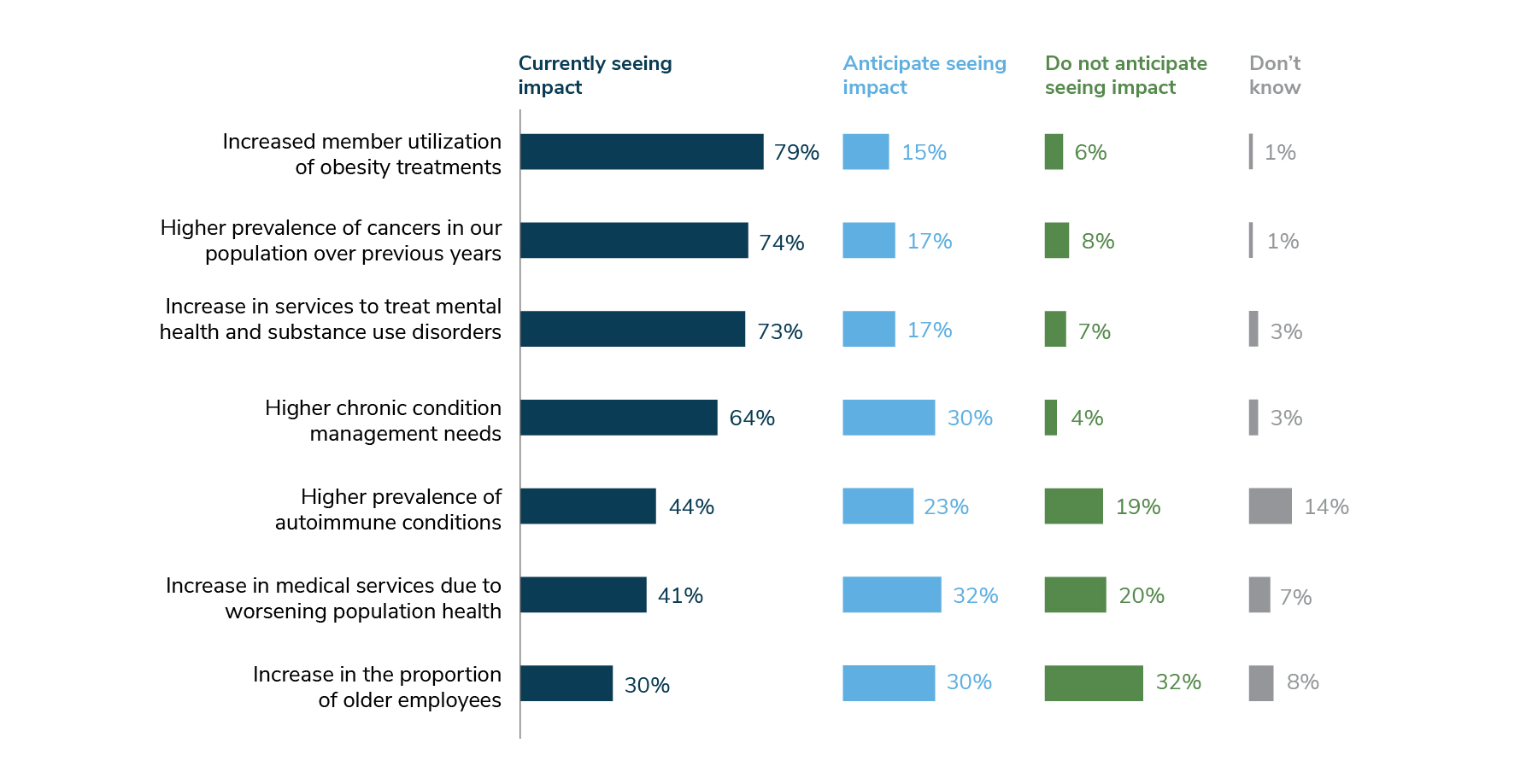

This year, employers have observed a number of factors that have tremendous implications for both near-term and future plan costs. More employers say that increases in obesity treatments (e.g., GLP-1s) are driving health care costs. In addition, employers reported an increase in the prevalence of cancer and higher utilization of mental health services. These and other market elements combine to drive up both the unit cost and utilization of health care services. Employers and employees must work together to address affordability in a multitude of ways. - For example, employers must assess the effectiveness of benefit provisions, programs and vendors offered, eliminating those that deliver less value, while employees can find cost-effective ways to get their recommended screenings and immunizations and use health plan resources and navigation tools to find providers that deliver high-value care.

-

Figure 2: Employer Experiences with Health and Well-being Trends, 2025

Figure 2: Employer Experiences with Health and Well-being Trends, 2025 -

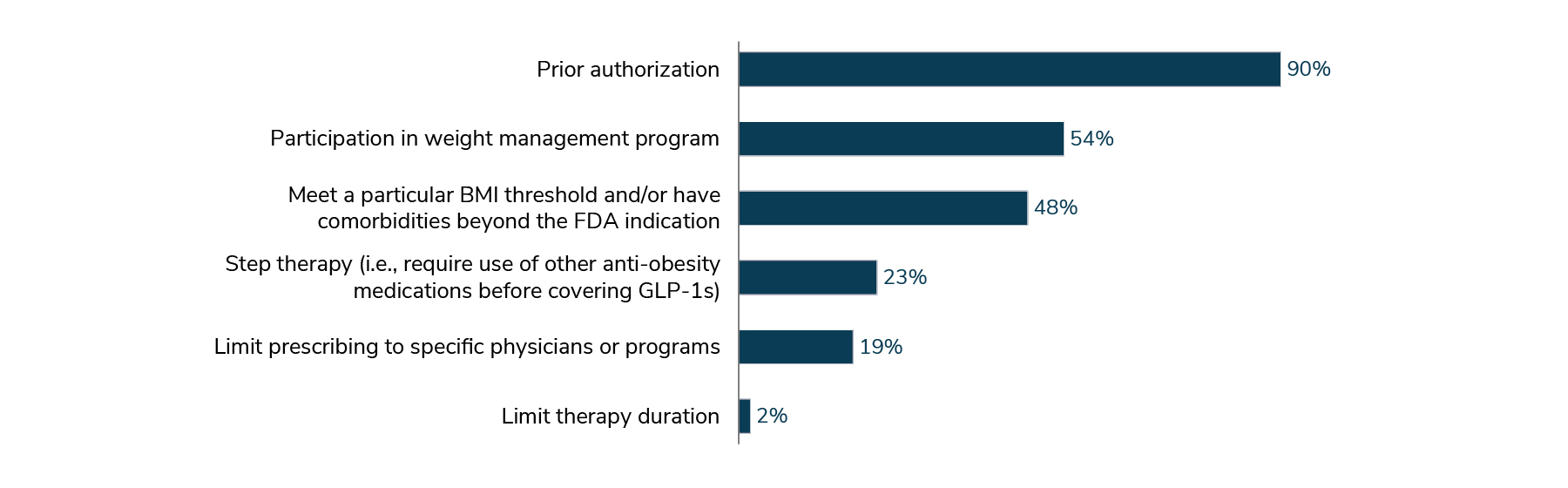

3 | Employers are seeing an increase in utilization of costly obesity medications, which play a role in overall health care cost increases. As a result, many employers are implementing prior authorizations and clinical oversight to address appropriateness and optimize outcomes. However, the high price of these popular medications continues to present a challenge.

As seen in Figure 2, 79% of employers are currently seeing an increase in the utilization of obesity medications, and an additional 15% are anticipating seeing an increase in the future. As discussed later in this report, the percent of employers covering GLP-1s for conditions other than diabetes will stagnate as employers try to stabilize their health care costs. More employers covering GLP-1s for obesity will place requirements such as prior authorization, participation in a weight management program and obtaining the prescription from a specific provider in order to ensure appropriateness and optimize outcomes for the patient and the plan.

Many employers face challenges when seeking to implement obesity management protocols; rebates related to GLP-1s are either reduced or eliminated under certain circumstances. As such, employers will need to require their vendor partners to deliver sustainable, cost-effective financial models for this class of medications or enable employers to implement utilization strategies of their choosing and receive the rebates earned.

Figure 3: Requirements for GLP-1 Coverage for Obesity, 2025

Figure 3: Requirements for GLP-1 Coverage for Obesity, 2025 -

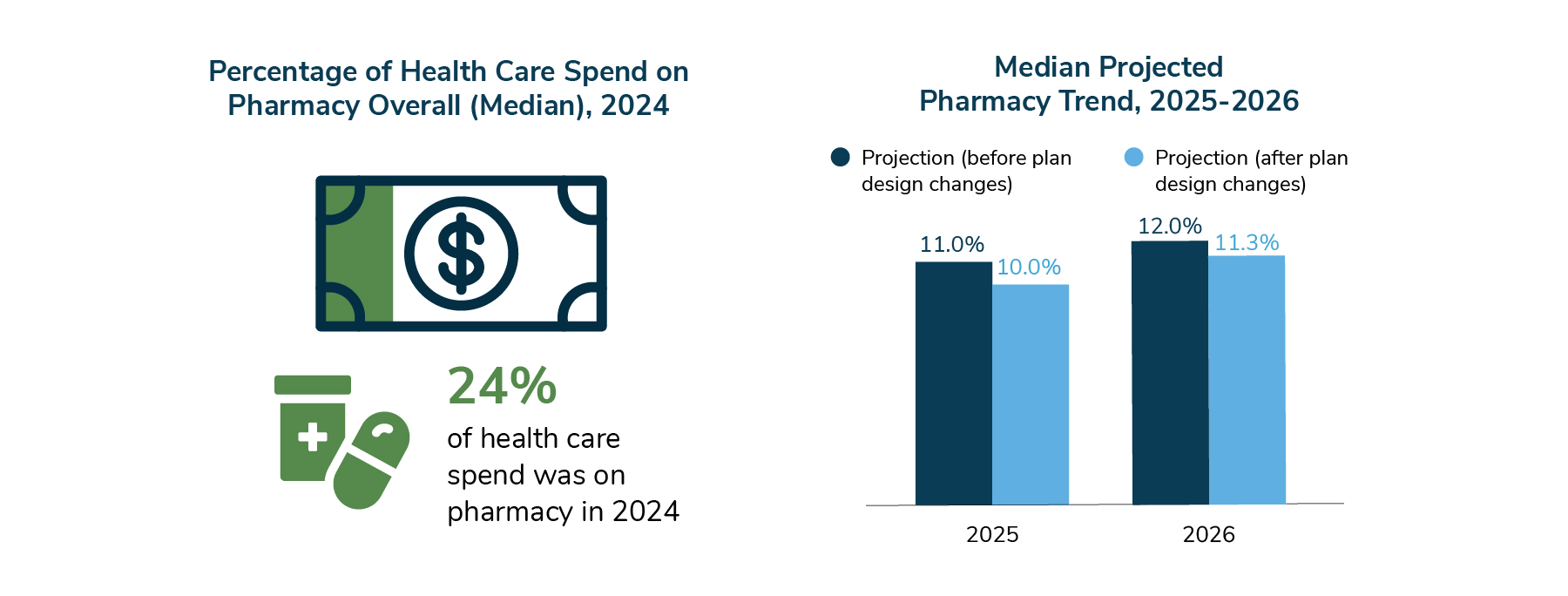

4 | A macro-level overhaul of the pharmacy supply chain is needed to address pharmaceutical costs for employers and employees. Even though a majority of employers use plan design approaches and utilize management strategies offered by their PBMs, pharmacy cost pressures are increasing, requiring more strategic approaches and systemwide reforms.

Fallout from the current macroeconomic environment, including potential tariffs, proposed changes to Medicare and Medicaid and other dynamics at play in the pharmaceutical market, means that employers are anticipating the cost of pharmaceuticals to continue to rise. This is on top of an already burgeoning pharmacy cost situation: In 2024, 24% of health care dollars went to pharmacy expenses. Employers are anticipating an 11-12% increase in their pharmacy costs in 2025 into 2026. This is not – and has not been – a situation that can be remedied by plan design changes. Employers must immediately explore implementation of non-traditional PBM models offered by incumbents and innovators alike, which focus on increased transparency and reduced reliance on rebates. Further, systemic change—whether brought on by dramatic marketplace moves or via government intervention—is necessary to bring down pharmacy costs for employers and employees alike.

Figure 4: Pharmacy Cost Trends, 2024-2026

Figure 4: Pharmacy Cost Trends, 2024-2026 -

5 | U.S. health care costs are impacting multinational employers’ ability to offer benefits outside the U.S. – and global health care costs are a growing concern.

For multinational employers, the impact of skyrocketing health care costs doesn’t stop at the U.S. border. When asked about rising U.S. health care costs’ impact on global benefits, 67% of multinational employers agree it affects what’s offered worldwide (Figure 5). When asked about their concern about controlling health care costs outside the U.S., three-quarters of multinational employers indicated some level of concern; 34% have the strongest level of concern. Cancer, musculoskeletal conditions, cardiovascular issues and diabetes were listed as cost drivers of concern worldwide.

Figure 5: Impact of Rising U.S. Health Care Costs on Global Benefits, 2025

Figure 5: Impact of Rising U.S. Health Care Costs on Global Benefits, 2025 -

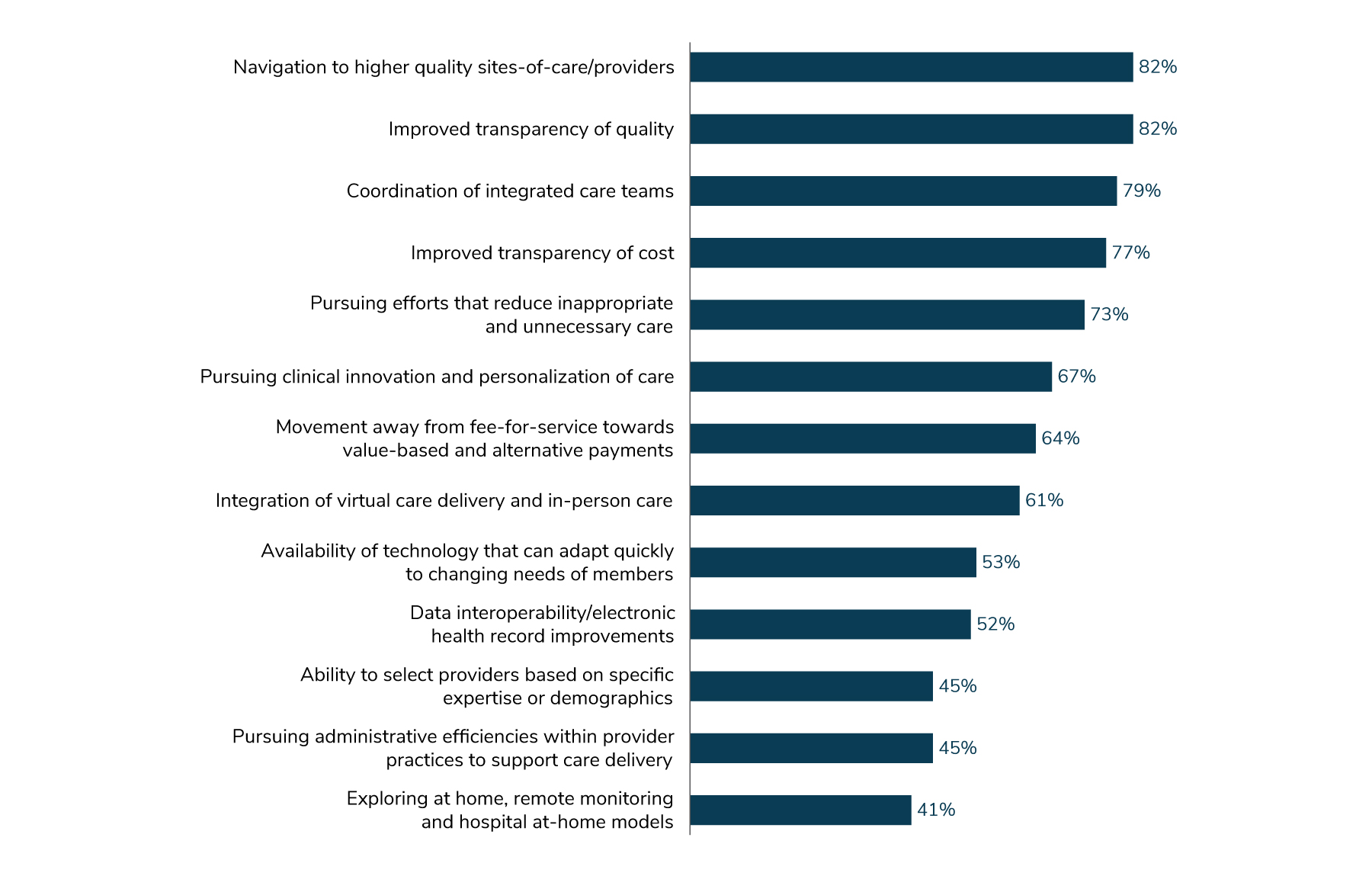

6 | Employers need to increase their focus on value while driving change to improve the quality of care that their employees receive. Crucial to this effort: Employers holding their vendors increasingly accountable for outcomes and tasking them with bringing forward bold ways to improve care while strengthening the employee experience.

By ramping up their focus on value-driven strategies and models, employers have a number of opportunities to improve the quality of care. Navigation to higher quality providers, improved transparency of quality data and coordination of integrated care teams top the list (Figure 6). However, these actions are dependent on partners’ ability to bring forward effective and bold ways to promote and enable value-based care.

As discussed later in the report (Figure 3.4), value-driven strategies include various approaches: centers of excellence, advanced primary care models and adoption of high-performance network models, including those offered through alternative health plans. While the number of employers deploying these strategies remains stable, opportunities exist to improve relevance and reach of these programs through broader enrollment and utilization.

While employers seek to accelerate their efforts in these areas, industry partners providing these services will need to accelerate progress in getting employees to higher value care, which can lower overall health care costs and improve experience.

Figure 6: Actions to Impact the Quality of Care, 2025

Figure 6: Actions to Impact the Quality of Care, 2025 -

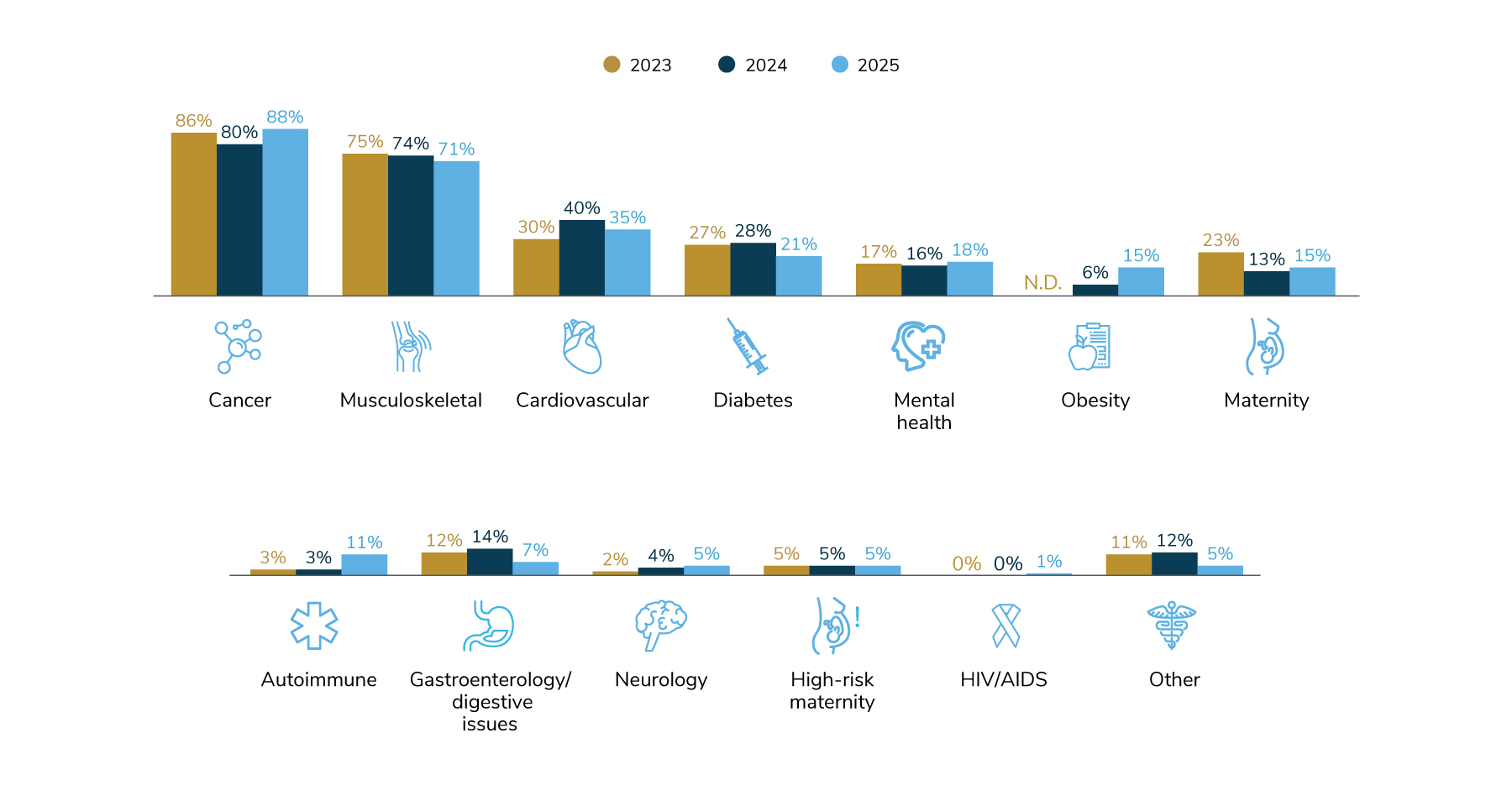

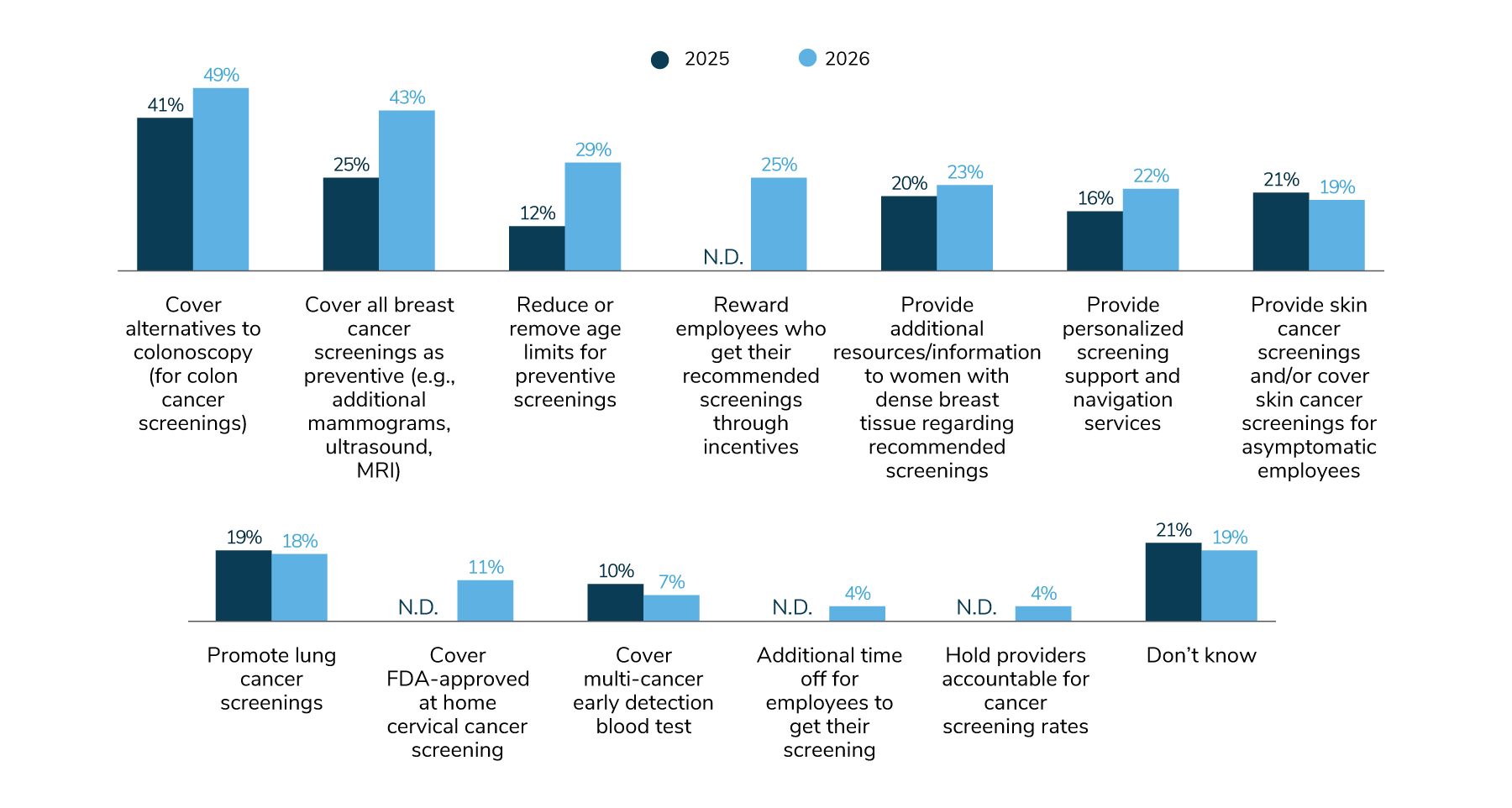

7 | Cancer continues to be the top condition driving employer health care costs, made worse by a growing prevalence of cancer diagnoses and the escalating costs of treatment.

For the fourth year in a row, cancer is the top condition driving health care cost, which is growing at an astounding rate. Accordingly, employers are doubling down on cancer prevention and screening coverage. More employers have enhanced their screening coverage, including covering alternatives to colonoscopies, expanding coverage of breast cancer screenings and removing age restrictions to preventive care coverage. Some employers are even providing personalized support to help employees understand which cancer screenings they are due for and rewarding those who follow through on recommendations. While prevention is key to getting ahead of the cancer cost curve, employers recognize that offering access to high-value treatments is also essential. About half of employers will offer a cancer COE in 2026, and another 23% are considering doing so by 2028.

Figure 7: Conditions Driving Costs, 2023-2025

Figure 7: Conditions Driving Costs, 2023-2025

Figure 8: Cancer Screening Measures, 2025-2026

Figure 8: Cancer Screening Measures, 2025-2026 -

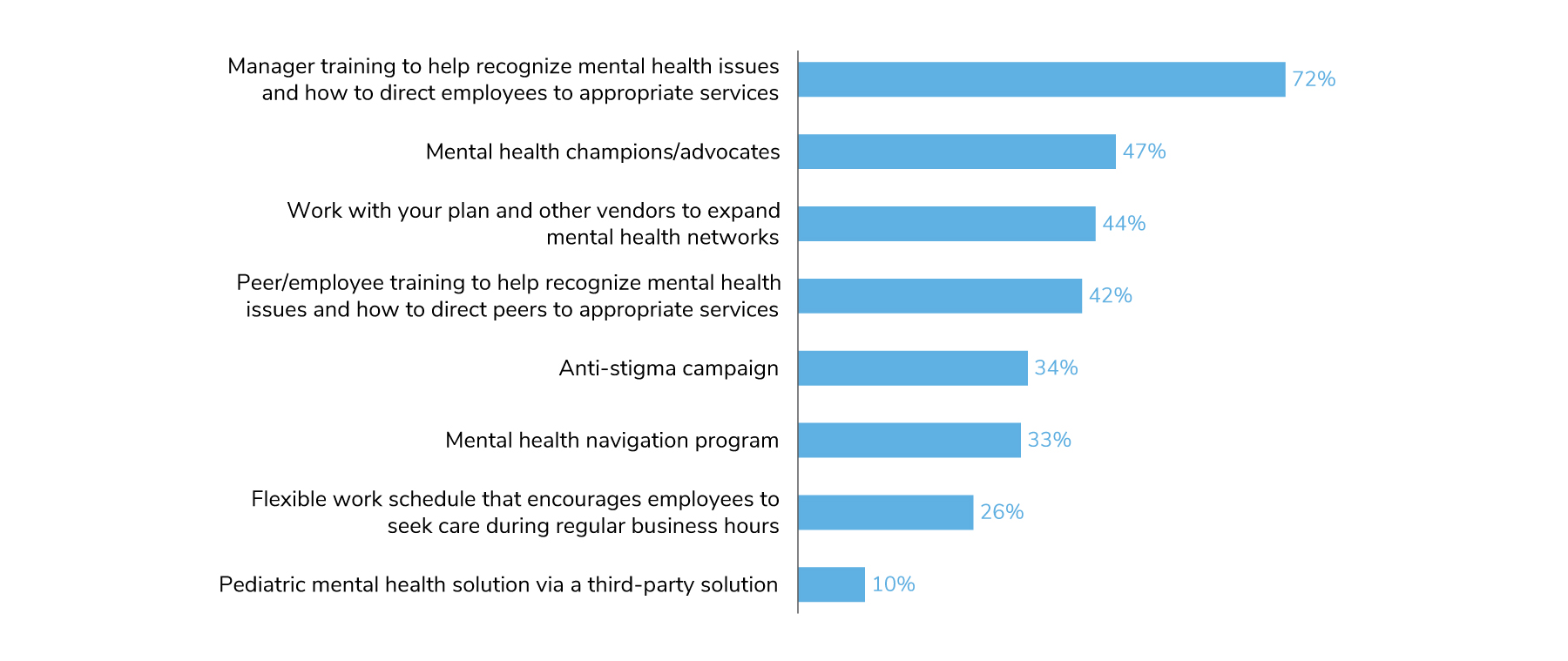

8 | A vast majority of employers have seen an increase in mental health services used by employees, resulting in mental health emerging as a cost driver. While employers continue to seek ways to expand access, they are also turning their focus to ensuring that these services are high quality and appropriate.

As illustrated earlier in Figure 2, 73% of employers reported an increase in mental health and substance use disorder services, and another 17% anticipate an increase in the future. Over the past few years, employers have been acutely focused on expanding access to treatment and support, through anti-stigma campaigns and the use of the growing number of virtual channels. The increase in utilization is probably a reflection of these employers strategies and employees availing themselves of these services. With improvements in access and utilization rates high, employers should now focus more on unit cost and high-quality, appropriate treatment to ensure that employees are getting the right mental health support at the right time and for the appropriate duration.

Figure 9: Strategies to Address Mental Health, 2026

Figure 9: Strategies to Address Mental Health, 2026

Health Benefits at a Crossroads: A Call for Bold Action for Employers

Heading into 2026, employers will need to navigate mounting health care costs, evaluate a growing array of solutions and consider new technologies and AI, which are disrupting many facets of health care. These concerns are set against a backdrop of an uncertain macroeconomic environment and a constantly evolving regulatory landscape, as well as pressures elsewhere in the health care landscape. This once-in-a-generation combination of events places employers at a crossroads. Employers need to take broader and bolder actions for themselves and their workforce. Industry partners and service providers need to intensify and accelerate efforts to support employers in navigating this new reality.

Considerations for employers and their partners include the following:

- Explore innovative models for health benefit management.

Many alternative health plans—offered by newer entrants and incumbents—infuse principles of driving value into their network designs, with a focus on advanced primary care and member navigation. Employers are looking to these models to drive greater value in the health care delivery system and make it easier for employees to access affordable, high-quality care. - Be open to emerging solutions and new pharmacy benefit management strategies.

There is room for collaboration with willing partners on high-priority pharmacy topics, including the following:- Increasing biosimilar adoption;

- Adopting an obesity management strategy that is not dictated by GLP-1 prices and related rebates; and

- Instituting stricter coverage and utilization criteria for high-cost therapies to ensure long-term sustainability and patient benefit.

- Call on consultant partners to comprehensively assess and explain alternative health plan and PBM models, including financial implications and participant change management.

While employers have seen only modest progress in the development of alternatives to traditional PBM models, some employers have already started to embrace existing alternatives offered by new vendors as well as emerging models offered by incumbent vendors. Employers have also begun to explore health plan variations. Employers should look to their consulting partners to effectively measure the financial impact of these alternatives and to craft compelling change management approaches to ease employer concerns about participant disruption. - Hold vendors accountable for performance—and eliminate underperforming programs.

Trusted vendors and programs that consistently demonstrate the value of their services and effectively manage costs will be necessary to improve quality and manage rising costs into the future. However, employers must hold vendors accountable—through renegotiating terms or changing vendors—if programs are not delivering outcomes. - Steer employees toward high-quality providers.

Employers should implement strategies that promote higher quality, including various approaches to centers of excellence, advanced primary care models and adoption of high-performance network models. Some of these strategies can help bring about immediate cost savings, but they all work to improve quality and reduce costs over time. - Encourage vendors to detail and demonstrate how artificial intelligence (AI) and data can support employers’ goals.

There are opportunities for the use of data and new solutions—including AI—to have a positive impact in employer health and well-being. Currently, AI is mostly utilized for communications and benefit administration within employer plans. However, employers can work with their partners to evaluate future opportunities to leverage new technology. - Multinational employers should evaluate the implications of rising health care costs in the U.S.—and globally—on their multinational strategy and ability to offer benefits worldwide.

Rising health care costs—particularly but not limited to the U.S.—constrain what multinationals can accomplish with their global benefits strategy. Even within those constraints, multinationals can still leverage programs, quality care, minimum standards and captive arrangements to manage global health care.

A Call to Action for Vendors and Partners

Employers won’t be able to take these bold leaps in a vacuum: They need trusted partners to evolve and innovate with in order to deliver meaningful change.

Vendors and partners need to become more proactive in their support of employers. The following recommendations provide a roadmap:

- Integrate and promote clinical solutions that deliver on quality and cost.

Health plans have the opportunity to promote high-value clinical solutions within their provider networks. Selection and contracting with those in-network solutions must be focused on quality of care delivered to the patient and value delivered to the employer. If a program or network solution fails to deliver, it may be time to part ways with the vendor. - Mental health service providers should focus on improving measurable quality and appropriate levels of care.

As a growing cost driver, partially due to successful efforts to increase access and reduce stigma, mental health presents an area of opportunity for addressing health care spending by focusing efforts on appropriateness and quality of care. Mental health solution providers need to evolve their offerings to more effectively match the care needs of patients with clinically appropriate levels of care, providing employers with reporting on quality outcomes. They should also work to help members progress appropriately through levels of care, and where possible, create capacity for more acute/urgent situations by advancing others to less frequent or prolonged durations of care. - Present bold solutions to address rising pharmacy costs.

Consultants and disruptors can fill the trust and solutions gap in the pharmacy space by demonstrating clear cost savings and better predictability of cost in alternative models. As employers look to address these challenges, they will look to new and incumbent partners. - Proactively detail and demonstrate—with proof points—how AI and data can support employers’ goals.

New technology—including AI—present opportunities to address many health and well-being challenges. Before the use of AI can become more widespread by employer benefits strategists, its value needs to become more clearly articulated, illustrated and validated. - Deliver promised outcomes—with supporting data—as employers narrow their partnerships to focus on consistently well-performing programs.

With health care costs rising, employers will focus on solutions that can prove that they are delivering their promised outcomes. Vendors/programs that can’t consistently demonstrate the value of their services may be at risk. Consultants and advisors must comprehensively articulate, demonstrate and thoroughly evaluate emerging models alongside existing models and work with employers to clearly articulate the opportunities and support them in developing the business case for transition when necessary. Consultants and advisors must also recognize when historical evaluation tools need to be modified to fairly and properly assess new models that do not fit into legacy frameworks. Vendors and partners under scrutiny need to clearly articulate the value of their offerings, providing robust data and validation of clinical and service outcomes.

Citations

Before referring to or using this survey report in any way, you must receive permission from Business Group on Health. Please contact [email protected].

Suggested citation for this survey report:

Business Group on Health. 2026 Employer Health Care Strategy Survey. August 2025. Available at: https://www.businessgrouphealth.org/resources/2026-Employer-Health-Care-Strategy-Survey.

-

Intro2026 Employer Health Care Strategy Survey

-

Executive Summary2026 Employer Health Care Strategy Survey: Executive Summary

-

Part 1Health Care and Pharmacy Costs

-

Part 2Health Care Strategy and Plan Management

-

Part 3Health Care Delivery

-

Part 4Health Care Program Design

-

Part 5Pharmacy Strategy and Design

-

Part 6Health Care Policy Perspectives

-

Part 7Global Health Care Costs

-

Full Report2026 Employer Health Care Strategy Survey: Full Report

-

Chart Pack2026 Employer Health Care Strategy Survey Chart Pack